A simple and practical guide for starters

Most people hear about interest rates when borrowing money or saving, but rarely stop to understand what they actually are or why they matter. Yet interest rates sit at the center of how modern economies function. They influence the cost of borrowing, the return on savings, and the overall flow of money in an economy.

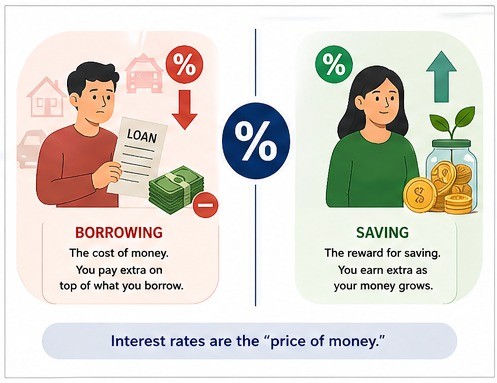

An interest rate is the cost of borrowing money or the reward for saving money, expressed as a percentage over a period of time.

If you borrow money, the interest rate determines how much extra you repay on top of what you borrowed. Whether you save or invest money determines how much your money grows over time.

In simple terms, interest rates are the “price of money.” Sounds weird, right? But its true, money has a price too.

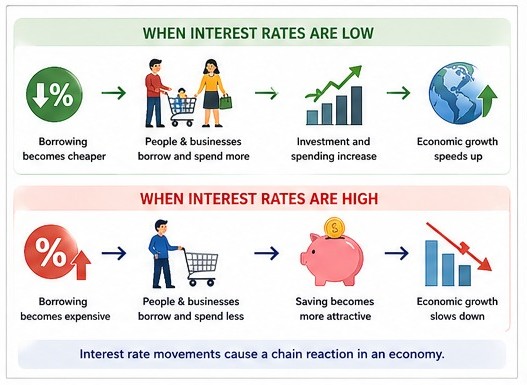

Interest rates matter because they control financial behavior at both individual and economic levels. They can be high or low, and that directly affects the decisions we make about money. Even if you think you ain't affected, someone else is, and it comes back. So basically, interest rate movements cause a chain reaction in an economy.

When interest rates are low, borrowing becomes cheaper, so people and businesses are more likely to take loans, spend, and invest. When interest rates are high, borrowing becomes expensive, so spending slows down and saving becomes more attractive.

This balance affects everything from personal loans to business expansion, housing markets, inflation, and overall economic growth.

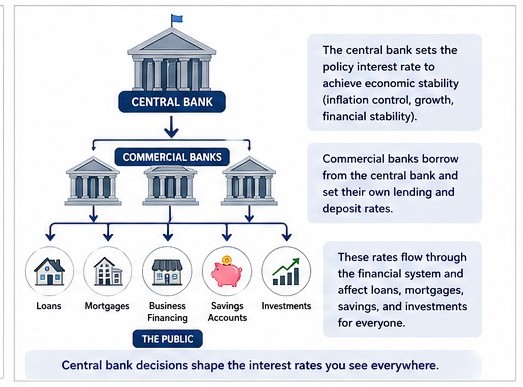

In most economies, central banks are responsible for setting or guiding interest rates. Examples include institutions like national central banks that manage monetary policy.

A central bank is essentially the “control center” of a country’s money system. Its main role is to keep the economy stable by managing inflation, encouraging growth, and maintaining trust in the financial system.

One of its main tools is the policy interest rate, which influences how much commercial banks charge each other for money. This then spreads through the entire financial system, affecting loans, mortgages, business financing, and savings rates offered to the public.

So even if you don’t deal with the central bank directly, its decisions quietly shape the interest rates you see everywhere else.

Understanding interest rates is not just for economists or bankers. It directly affects everyday financial decisions.

Whether you are borrowing money, saving, investing, or running a business, interest rates determine how much you gain or lose over time. Ignoring them means you are making financial decisions without understanding the real cost or return involved.

In simple terms, if you don’t understand interest rates, you don’t fully understand the price of money.

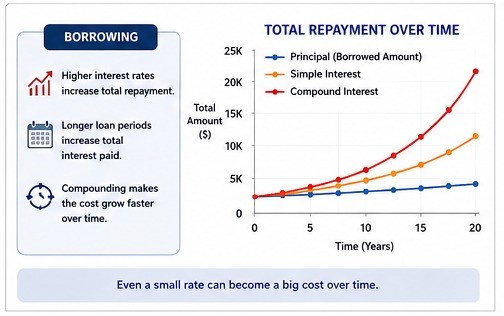

When you borrow money, the interest rate represents the cost of debt. It determines how much extra you pay over time in addition to the original amount borrowed.

But what really matters is how that interest is applied. Some loans use compounding, which means interest is calculated not only on the original amount, but also on accumulated interest over time.

This is why loan repayments can grow significantly over longer periods. Even if the rate looks small, compounding can increase the total repayment amount.

In practical terms:

• Higher interest rates increase total repayment.

• Longer loan periods increase total interest paid.

• Compounding makes the cost grow faster over time.

This is why the structure of the loan matters just as much as the rate itself.

For savings, interest rates work in the opposite direction. Instead of costing you money, they generate returns.

When you save money in a bank or invest in interest-bearing instruments like bonds, treasury bills, or CDs, the interest rate determines your earning potential.

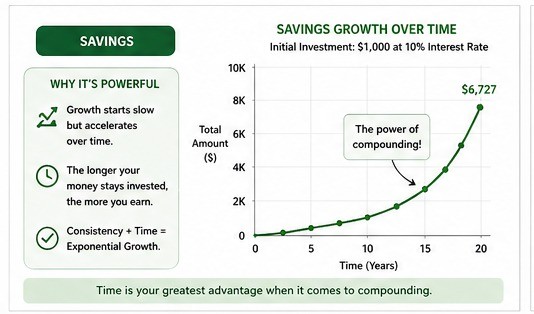

Most savings systems also use compound growth, meaning you earn interest not only on your original savings, but also on previously earned interest. Over time, this creates exponential growth rather than linear growth.

This is why long-term saving is powerful. The longer your money stays invested, the more compounding works in your favor.

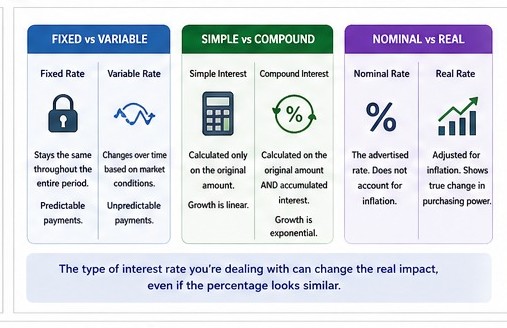

Interest rates are not all the same, and this is where things start to get more practical. The type of interest rate you’re dealing with can completely change how much you pay or earn, even if the percentage looks similar at first glance.

One of the most common distinctions is between fixed and variable interest rates. A fixed interest rate stays the same throughout the entire period. If you borrow at a fixed rate, your payments remain predictable because the cost of borrowing does not change. This stability is useful, especially over long periods, because it protects you from unexpected increases.

A variable (or floating) interest rate, on the other hand, changes over time. It is usually tied to broader economic conditions or central bank decisions. This means your cost of borrowing can go up or down depending on what is happening in the economy. At times, this can work in your favor if the rates fall, but it also introduces uncertainty. What starts as a low rate can increase and make repayments more expensive over time.

Another important distinction is between simple interest and compound interest, and this is where many people underestimate the real impact of interest rates.

Simple interest is calculated only on the original amount. It is straightforward and predictable because the interest does not build on itself.

Compound interest, however, works differently. It is calculated on both the original amount and any accumulated interest. Over time, this creates a snowball effect. For borrowing, this means the cost can grow faster than expected. For saving or investing, it means your money can grow much faster, especially over long periods.

Then there is the difference between nominal and real interest rates. A nominal interest rate is the rate you see advertised. It does not account for inflation. A real interest rate adjusts for inflation and shows the true change in purchasing power.

This distinction matters because a high nominal rate does not always mean you are gaining in real terms. If inflation is also high, the actual value of what you earn or repay may not change as much as it seems.

All these types show one thing clearly: the percentage alone is never the full story. The structure behind the interest rate is what determines its real impact.

You cannot completely avoid interest rates; they are part of any financial system, but you can control how much they affect you by making more informed decisions.

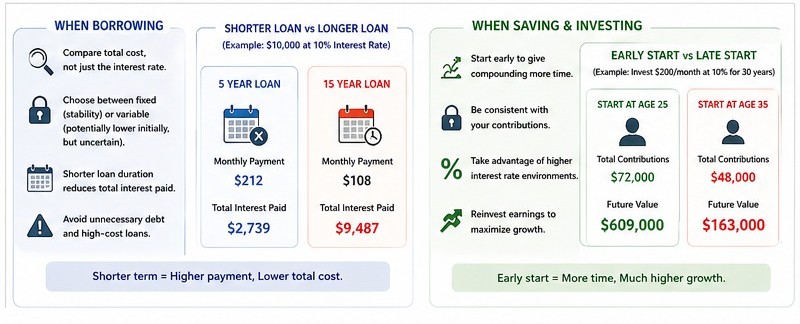

When it comes to borrowing, the first step is to stop looking at the interest rate as just a number and start looking at the total cost. Comparing lenders helps, but only if you understand how their interest is structured. A lower rate with unfavorable terms can sometimes cost more than a slightly higher rate with better conditions.

It also helps to pay attention to whether the rate is fixed or variable. Fixed rates give you predictability, while variable rates carry risk. Choosing between them depends on whether you value stability or are willing to take on uncertainty for a potentially lower initial cost.

Loan duration is another major factor. The longer you take to repay a loan, the more time interest has to accumulate. Even if the payments feel smaller, the total amount paid over time is usually higher. Shorter terms may feel heavier in the moment, but they often reduce the overall cost significantly.

Avoiding unnecessary debt is just as important. High-cost, quick-access loans may seem convenient, but they often carry structures that make them expensive over time. Understanding this upfront helps you avoid situations where interest works against you.

On the savings and investment side, the goal is to make interest work in your favor. This is where compound growth becomes powerful. The earlier and more consistently you save, the more time your money has to grow on its own.

Consistency matters more than timing. Regular contributions, even small ones, allow compounding to build momentum over time. At the same time, paying attention to interest rate environments can help you take advantage of better returns when they are available.

In both borrowing and saving, the key idea is the same: don’t just accept the interest rate at face value. Understand how it behaves over time and how it interacts with your decisions.

Interest rates are more than just numbers attached to loans or savings. They are a core part of how money moves through the economy and how financial decisions are shaped.

They determine the cost of borrowing, the reward for saving, and the pace of economic activity. Once you understand how they are set, how they work, and how they affect compounding, you begin to see that interest rates are not just financial details; they are financial drivers.

Understanding interest rates does not just make you more informed. It helps you make better decisions with money in almost every area of life.